To read the full report on Tucson’s Office market activity in Q1, click here

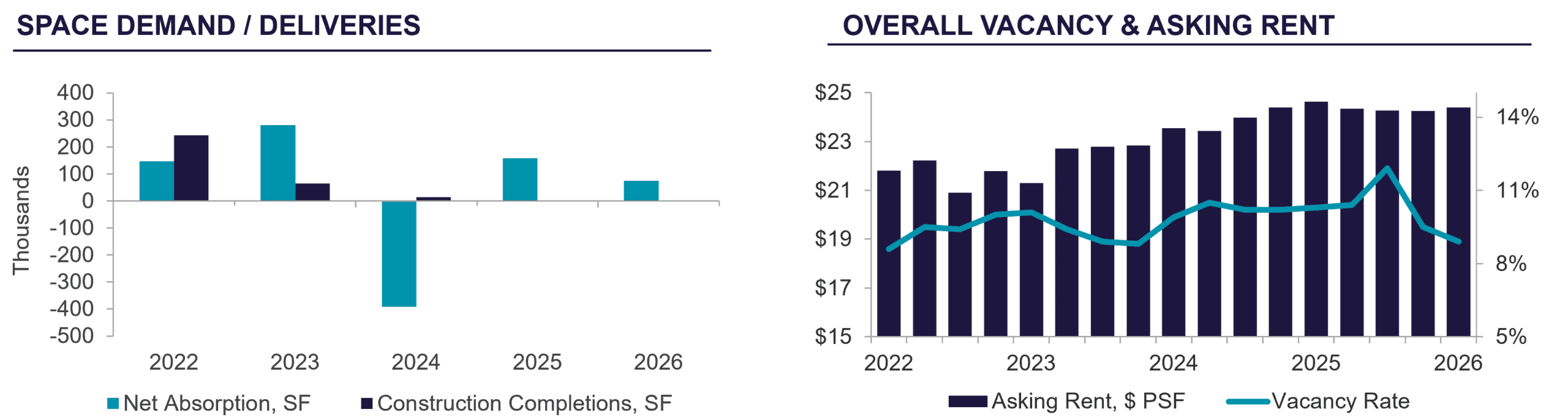

In Q1 2026, Tucson’s office market posted modest gains, with vacancy declining to 8.9% as leasing activity improved. Approximately 320,000 square feet (sf) was leased, contributing to year-to-date net absorption of 69,726 sf. While vacancy remains above equilibrium, overall demand showed measurable strengthening.

Healthcare continued to serve as the primary driver of activity, with additional contributions from financial and education users. Performance across submarkets remained uneven but favorable in select areas. The Northwest, Southwest, Foothills, and Downtown submarkets outperformed the broader market, maintaining low vacancy levels between 2% and 6% and attracting most of the tenant interest.

Development activity remained constrained. No new product was delivered during the quarter, and approximately 116,788 sf remains under construction. Elevated costs continue to limit speculative development, prompting increased interest in repositioning existing assets. The former Geico facility at 930–950 N Finance Drive exemplifies this trend, with its recent sale expected to lead to redevelopment.

Rental rates increased modestly in Q1, with average asking rents reaching $24.39 per square foot (psf). Market conditions reflected a relatively balanced negotiation environment though landlords continued to offer concessions consistent with a tenant-favorable landscape. Lease terms typically ranged from three to five years, with tenants prioritizing quality space in well-located submarkets.

Sales activity remained measured but stable, with average pricing near $150 psf, slightly above prior levels. Notable transactions included the sale of 155 North Rosemont, a 51,404 sf asset near the Williams Centre, which traded at approximately $169 psf. Investor activity continued to favor medical and healthcare-related assets, while broader economic uncertainty, including inflationary pressures, has tempered overall transaction volume.