To read the full report on Tucson’s retail activity in Q4, click here.

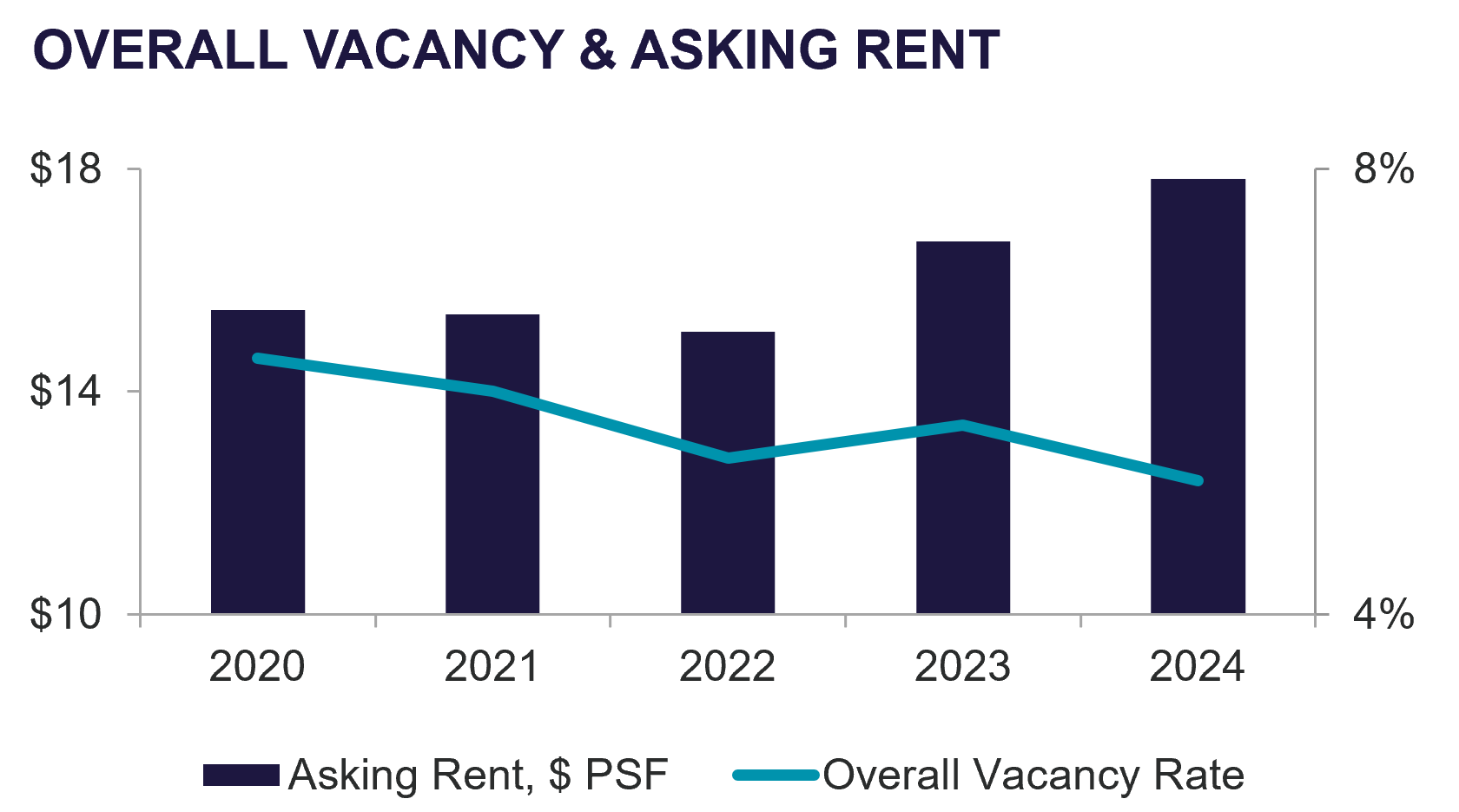

The Tucson retail market experienced a slight uptick in vacancy, reaching 5.8% in Q4 due to the closure of Big Lots and 99 Cent Only stores. Class A properties continue to command historically high lease rates, with rents in the mid $40.00 per square foot (sf) triple-net (NNN) range common for new construction and projected to rise further in the coming year.

Restaurants, health and wellness/fitness establishments and ‘medtail’ concepts remain the most active users in the market. The Foothills, Oro Valley, Vail, and Marana submarkets continue to be highly desirable to retailers, maintaining minimal vacancy, some as low as 1.9%.

Notable lease transactions included a 149,900 sf Fry’s in Marana, Walmart’s expansion of 86,922 sf at Tucson Place, and a new pickleball business leasing 30,162 sf in the Oro Valley Marketplace. Key sale transactions included the retail portion of Oracle Gateway shopping center selling for $7.1 million to an investor, a 21,440 sf Walgreens property in East Tucson changing hands for $2.05 million, and an investor acquiring 15,261 sf building for $1.6 million, also in East Tucson.

Both Investment and user sale activity and pricing remained relatively stable, with most transactions driven by users, particularly restaurants seeking prime pad locations or buildings suitable for redevelopment on corner sites. High interest rates and elevated cap rates continued to influence investor interest. Consumer spending saw a boost this quarter, attributed to holiday shopping, with food, beverage, and entertainment sectors performing strongly. An emerging trend of note was the repurposing of vacant big box stores for entertainment uses. The Roadhouse Cinema expansion from earlier this year exemplifies this shift, with plans to transform a former Bed Bath & Beyond space into an entertainment complex featuring bowling, Topgolf swing suites, and axe throwing.